We Work was symptomatic of venture capital funded companies that tiptoed to the public markets with no profits to feed the beast.

In the case of We Work, the market finally woke up and said, “Hey, you don’t even have a plan to become profitable. Get outta here.”

We Work was further punished for the behavior of its leader, the inimitable Adam Neumann, who was treated to a hubris-crushing cure that resulted in his departure (though anybody who gets bought out with a more than a billion dollar send off will get no sympathy in the Big Red Car’s book, sorry).

What has now taken root is the quaint notion that companies — even before going to the beauty parlor to get primped for an IPO — are going to have to be within earshot of being profitable.

I think the market has now had a bellyful of companies like Uber and Lyft and a number of others (SmileDirectClub) who are devoid of profits, but who feel like they should be public companies for reasons that are unfathomable.

We Work has put this logic into an unfavorable decline.

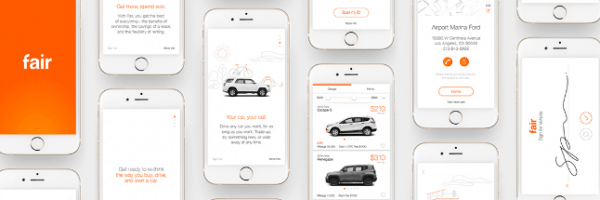

Comes now the curious case of Fair.

Let’s review the bidding, shall we?

1. Fair brings flexible car ownership to the marketplace. You pick a car and use it on a similar basis to a lease without any long term commitment by paying a monthly “rental” fee.

2. Fair provides you a car, roadside assistance, routine maintenance, a limited warranty, and the ability to add insurance — all with the signature of a fingertip. It is uber convenient. Ooops, can’t say “uber.”

3. You can “rent” a Yaris for $210/month or a 2018 BMW M3 for $1,310 per month.

It is a lot more complicated — mileage, excess wear and tear, registration, warranty — than just the three points above, but that is not germane to what I want to talk to.

So, Fair is valued at $1,200,000,000 with more than $500,000,000 of invested equity from SoftBank and others. There is also substantial debt.

So what, Big Red Car?

So, dear reader, $1,200,000,000 of value with $500,000,000 invested is not a great investment, is it? Doubling the value of the invested equity?

So, Fair has decided to take some pretty fierce medicine to get to profitability.

1. The whole dialogue at Fair has changed. They are now focused on profitability.

2. Fair is going to let 40% of their work force take a hike including the CFO, the brother of the CEO and co-founder.

3. It is a little foggy, but it appears that Fair is focused on growth by acquisition. Thy have made a couple of acquisitions.

4. The CEO of Fair, an industry stud, wants you to know that SoftBank is not “leaning” on them, but “supporting” them. [Your Big Red Car can’t help but think that SoftBank — after the We Work fiasco — is a little more careful these days when dealing with Unicorns whose numbers are not doing a conga line toward profit. Just me projecting. Could be wrong.]

I want to say one other thing. In much the same way that We Work was trying to convince you that they had made real estate into a SaaS business and therefore commanded and deserved SaaS-like multiples, it strikes me that Fair is just garden variety auto leasing with shorter terms.

It is still a car. It is still not full ownership — meaning you don’t buy the car. You still have mileage and wear & tear issues.

How is this not the auto leasing business, which is also not SaaS? It is garden variety auto fintech, maybe. [Caution, that could just be me projecting my anti We Work cat on the hot stove bias.]

Bottom line it, Big Red Car

OK, dear reader, I am not here to rain on Fair’s parade. But, I do observe that SoftBank — the big funder of We Work — is playing a more conservative tune here, and that this looks remarkably like auto leasing rather than SaaS in the auto business.

Could just be me.

But, hey, what the Hell do I really know anyway? I’m just a Big Red Car. Have a great week, y’all.